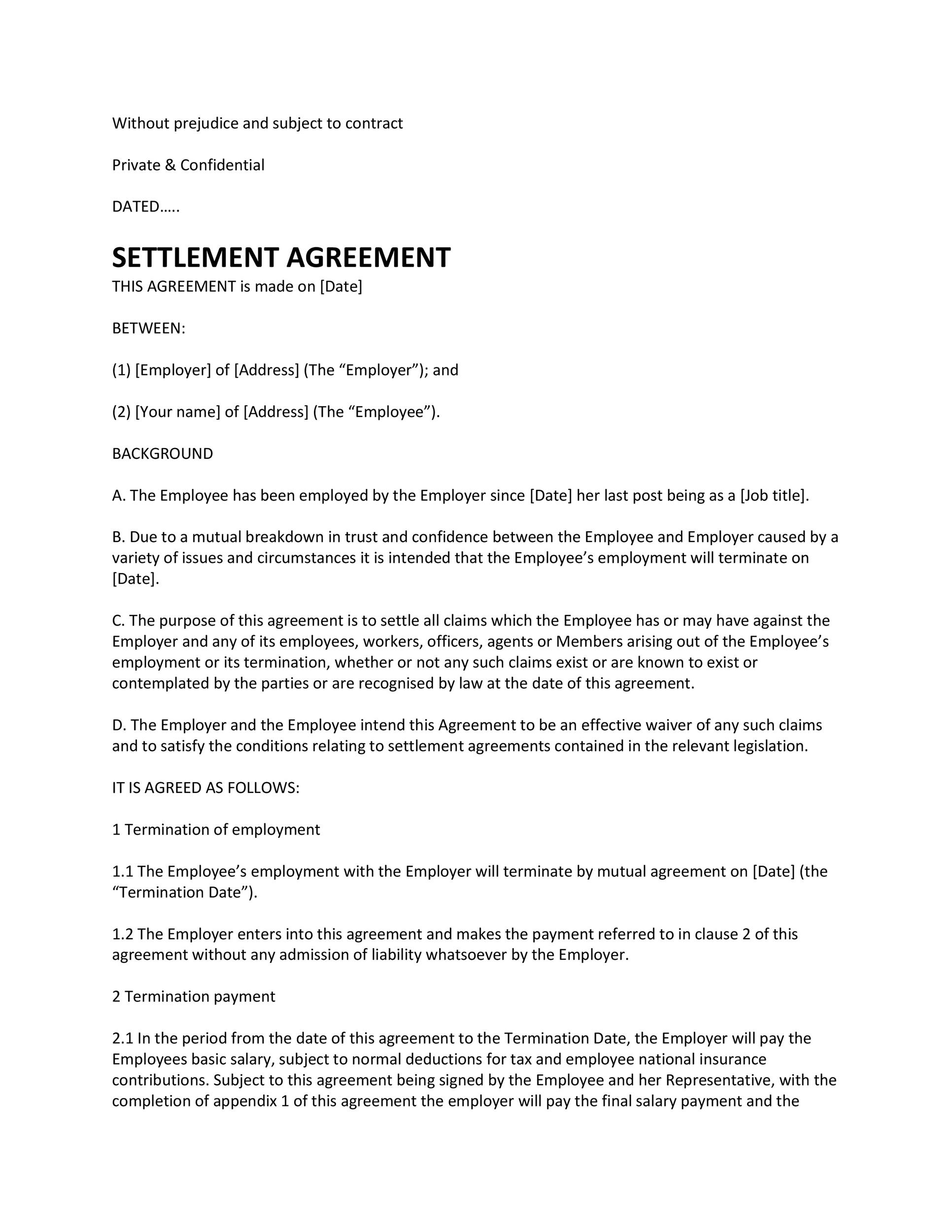

Immediately following contrasting pricing regarding various loan providers and you will finding the right fit, it’s time to safe their home loan price. A speed lock freezes the rate of interest and ensures your month-to-month money will still be stable regarding the closure process. Price locking is normally designed for doing 1 month within no extra rates, having choices to stretch.

Think of cash advance loans Echo Hills CO, if you are rates tresses shield you from ascending cost, however they mean you will never make use of one rate drops. not, certain lenders render a performance drift-off option, enabling you to conform to down rates of interest, potentially that have a fee, even in the event get a hold of software may offer it benefit without extra costs.

The way to get a minimal financial rate

Willing to have the reduced mortgage price? Regardless if you are looking to purchase a separate household or a resident refinancing an existing household, these finest information allows you to rating a lower interest rate!

Usually do not accept the original financial speed offer rating

Even if you think big date try of one’s substance, you will need to understand the prices most other lenders show up with. Rates of interest and you can lender costs notably feeling just how much you’ll spend, so it is important to be sure you’re going to get the best possible package.

If you settle for a high rate quickly, you can stop your self later on once you see most readily useful also offers. As an instance, just an excellent 0.25% high rate can add a supplementary $40 towards the monthly mortgage payment.

If you’re that might maybe not seem like a great deal, they adds up to over $thirteen,000 along the entire life of one’s mortgage. Focusing on how to purchase home loan pricing can help you prevent this costly error.

You should never default towards most recent bank because it’s effortless

Whenever finding out tips look for home loan costs, you are lured to continue your entire monetary deals that have your current financial in the interest of convenience. However, if they’re not providing you with a knowledgeable speed or the correct financing program for your individual earnings, you might be indeed best off protecting a mortgage from another financial.

Is huge banks, borrowing from the bank unions, on the web lenders, and even mortgage brokers to acquire the lowest attract price and greatest price.

Go ahead and, see just what your financial perform for you. Just don’t believe you will be compelled to stick to them to suit your mortgage. Of many financial institutions will actually sell the loan to help you home financing servicer anyhow, and that means you wouldn’t find yourself with them over the lives of your home financing.

Think to get down your interest

That it commission is normally indicated inside financial facts, with one-point equating to 1% of amount borrowed and you will probably reducing your rates of the 0.25%.

Example: Witn a good $three hundred,000 loan, to buy down your own price from the two factors do cost $six,000. Anyone who has additional upfront bucks and you can plan to remain in their house enough time-identity can save a quite a bit along the longevity of the mortgage, such having larger jumbo funds.

Assess the discounts having fun with home financing calculator and you may speak to your lender into the financing estimate way to know if this strategy can make financial experience to you personally.

Enhance your credit score and your down-payment

That is because a top credit rating indicators to loan providers that you’re a professional debtor, which can lead to lower prices. You might increase your borrowing from the bank if you are paying costs promptly, reducing financial obligation, particularly higher-desire credit debt, and repairing people credit file errors. Also, daily comment your credit score to relax and play any situations early.

At the same time, a more impressive down-payment reduces your perceived risk so you’re able to lenders, potentially resulting in lower interest rates. If possible, save your self a lot more for the deposit to minimize your loan count and you can possibly avoid private home loan insurance rates (PMI), which will help you save far more currency.