Quick mortgages try a switch notice of agency’s initiative

- Desk from Information

The latest U.S. Department out-of Houses and you can Metropolitan Development (HUD) when you look at the April put-out the Security Plan, geared apply for payday loan Dotsero towards getting rid of brand new racial homeownership gap and you will boosting security when you look at the homeownership to some extent because of the improving access to financial support having homeowners. The master plan falls under the newest Biden administration’s greater whole-regulators equity schedule together with very first regarding all casing or home loan firms are revealed this season.

Homeownership costs has risen across the board lately, nevertheless racial homeownership gap is at their largest in two an effective century. Centered on Pew’s study of You.S. Census Agency studies, the essential difference between prices from Black-and-white homeownership was 24 commission factors for the 1970 and you can 31 payment points when you look at the 2020.

The fresh HUD package calls for a variety of procedures to deal with the gap. It would control tech to alter the latest overall performance of the Federal Homes Administration (FHA) loan program while increasing home financing selection, one of almost every other initiatives. Importantly, they focuses on new minimal method of getting brief mortgage loans to buy low-rates site-mainly based and you can are built property because the a boundary to help you equitable homeownership and you can actions to improve the means to access money to own are produced casing.

Growing the availability of like mortgages together with may help relieve buyers’ reliance on riskier, costlier option money whenever attempting to purchase reasonable-rates belongings-people valued during the lower than $2 hundred,000. The alternative capital choices were residential property deals, seller-financed mortgages, lease-pick preparations, and personal property finance.

Specific homeowners move to choice capital to find reasonable-rates property partly on account of insufficient small mortgages, the individuals for less than $150,000. In the 2021, Pew used a first-ever before national questionnaire into option capital and discovered one thirty six million Americans have tried these arrangements will eventually-both more than once-to try and buy a house. Although some plans have more defense as opposed to others, as a whole, he’s got a lot fewer consumer defenses and higher will set you back than just mortgages.

Pew’s questionnaire found disparities inside dependence on choice funding of the competition, ethnicity, and money, showing inequities based in the housing marketplace alot more generally. Hispanic home individuals, specifically, are more inclined to have tried such agreements than nearly any almost every other battle or ethnicity.

Figure step 1

Lower-earnings individuals also are very likely to have fun with option funding. One of all the current individuals, those with yearly family profits not as much as $fifty,000 have been more seven minutes as the apt to be using option financing buying their homes than simply those with yearly household income of $fifty,000 or maybe more (23% in place of step 3%, respectively).

Profile 2

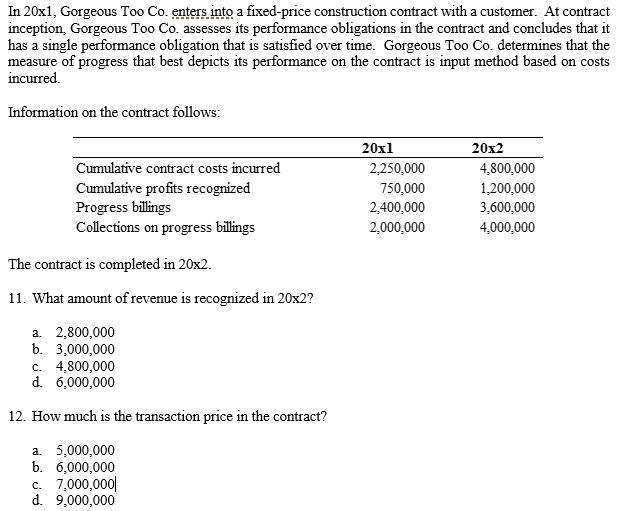

Reliance upon choice money is not, but not, a narrative from the money alone. The newest disproportionate the means to access these plans from the lower-earnings families reflects disparities during the access to mortgages. Traditional mortgage loans certainly are the gold standard home based financing as they normally have lower costs plus individual protections than other alternatives. Even when lowest- to help you modest-money domestic borrowers are more inclined to search lowest-prices homes, and ideally such property might possibly be funded which have a tiny mortgage, the only solution offered tend to turns out to be alternative financial support. One could be the scenario although borrowers was mortgage-ready, meaning they may reasonably qualify for and you can repay a mortgage.

Because the HUD listed, short mortgages are usually tough and you may pricey to have loan providers so you’re able to originate-no matter a good borrower’s money. And you can early in the day research has built that’s not while the applicants are maybe not creditworthy.

Boosting equity in the homeownership starts with short mortgage loans

Low levels out of short-home loan credit according to offered residential property disproportionately influences very first-date homebuyers, low- to help you modest-earnings household, and you will borrowers from color that happen to be apt to be than the others so you’re able to have confidence in short mortgages to find reduced-cost properties.

The easiest way to increase fair accessibility mortgage loans and reduce the new homeownership pit is through handling the barriers you to definitely limit short-home loan origination. Such as, the newest repaired can cost you so you’re able to originate home financing and you can lenders’ commission-mainly based payment impact the profitability regarding brief mortgages. You to definitely fact incentivizes loan providers to focus on large-equilibrium funds. Financial regulations, which can be had a need to cover borrowers, often offer these costs with the addition of to help you lenders’ compliance debt and you can contact with legal and reputational risk.

HUD’s propose to get to know systems to improve the available choices of brief mortgage loans and you may expand use of resource having are built construction could help scores of financial-able individuals which might if not consider riskier option capital. Given that company actions pass with its arrangements, personnel enjoys a chance to thought generally regarding the many ways Us citizens buy their houses and you will display screen making use of and disparities contained in this choice a mortgage.